White Papers

Gain insights into quantitative finance, real-time risk management and trading technology through Algorithmica’s expert white papers and research.

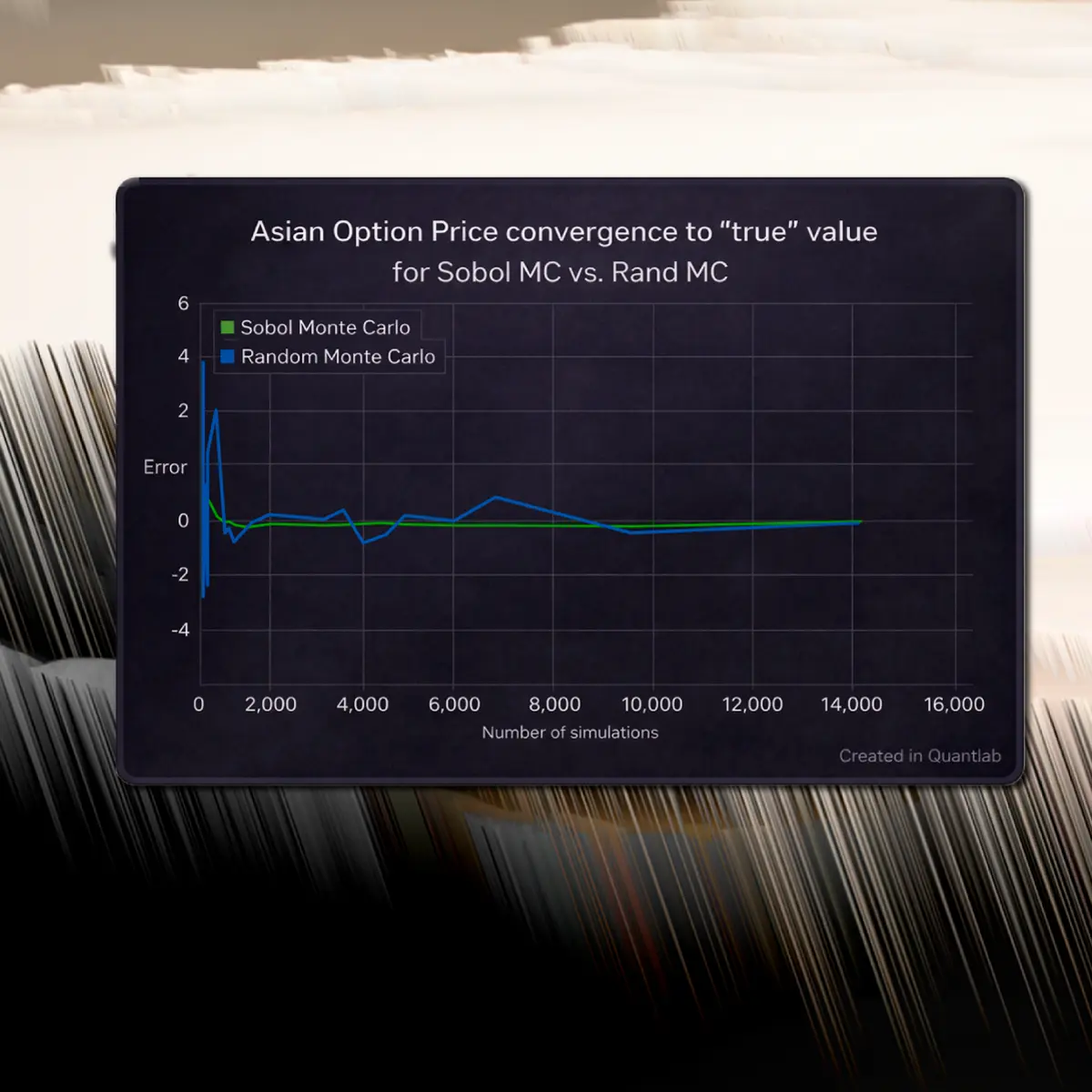

Improving Monte Carlo Convergence with Sobol Sequences

Discover how Sobol sequences can dramatically improve Monte Carlo convergence in quantitative finance. This white paper explains how quasi-Monte Carlo techniques reduce simulation noise, improve pricing stability and achieve accurate results with significantly fewer simulation paths.

Quantifying Currency Basis Spreads

for Accurate FX Valuation

This white paper explains how currency basis spreads arise, why “naive” discounting creates valuation errors, and how implied rates can be quantified to achieve more accurate FX pricing and risk management.