When pricing speed outpaces market reality

In most established trading organisations, the importance of low-latency pricing is already well understood. Over the years, desks have invested heavily in faster models, optimised infrastructure and increasingly sophisticated execution pipelines. Milliseconds matter, but only under one condition: that the inputs driving those models reflect the current market state.

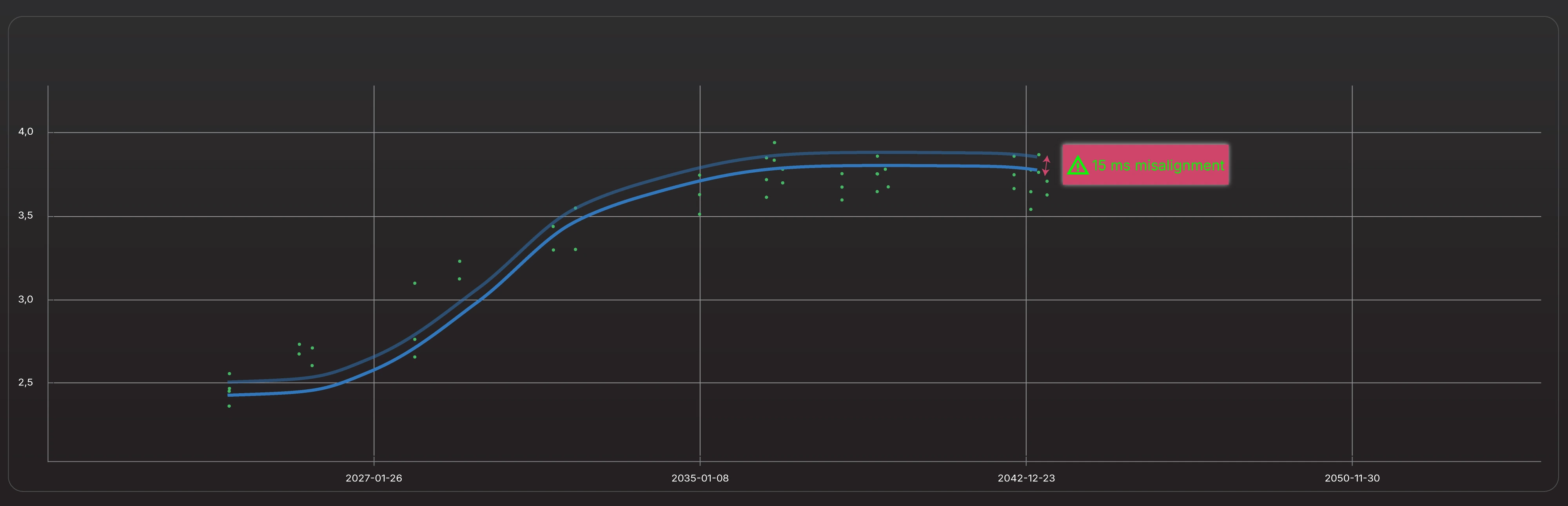

Curve latency is where this assumption quietly breaks down.

Even in well-run environments, curves may update less frequently than pricing models consume them. The discrepancy is often small, tens of milliseconds rather than seconds, yet in electronic fixed income markets that gap is material. Quotes may be generated quickly, but on a market representation that is already outdated. Over time, this degrades quoting quality and limits PnL in ways that are difficult to attribute to a single cause.

For senior practitioners, the more serious implication lies in risk. The moment a trade is evaluated, pricing and risk are implicitly coupled. First-order sensitivities all depend on the same curves that determine fair value. If those curves are stale or inconsistently calibrated, price and risk no longer describe the same market state. The result is not simply inaccurate numbers, but decisions made on internally inconsistent information.

In practice, addressing this issue seldom requires more modelling sophistication. It requires tighter engineering discipline around curve construction, calibration and delivery. In Algorithmica environments, this is typically achieved by treating curve pipelines as production-critical components, implemented using Quantlab Server and fully versioned in AHS (Algorithmica History Server). Curve states, calibration assumptions and update times are explicit, reproducible and aligned with downstream pricing and risk consumption.

Importantly, there is no universal curve solution. Instrument sets, liquidity profiles, data sources and governance requirements differ widely across institutions. For this reason, curve pipelines are almost always bespoke, even when they rely on common quantitative foundations. What matters is not uniformity, but coherence.

Low-latency pricing delivers value only when it is anchored in a market view that is both current and internally consistent.